When mortgage rates start flirting with 6%, Florida buyers tend to feel something they have not felt in a while: momentum. A slightly lower payment can move a home from “maybe” to “yes,” and it can bring more listings and more sellers back into the market.

There is also a real risk. When rates dip, buyers sometimes rush, overpay, or pick a loan structure that looks good today but hurts later.

The better move is to treat “under 6%” as a window, not a guarantee. Rates can move quickly. Lender pricing can vary by credit score, down payment, loan type, and points (fees paid up front to reduce the rate). Florida is also a local market. What is happening with Miami condos can look very different from Central Florida single-family homes.

This guide explains what “under 6%” really means, how it can affect Florida mortgage rates, and the smart ways to act if you are buying or refinancing in 2026.

Quick start: pick your path

- Florida first-time buyer

- Focus: buying power, step-by-step roadmap, common mistakes.

- Move-up buyer (selling and buying)

- Focus: timing strategy, concessions, rate locks.

- Refinance rates Florida shopper

- Focus: break-even math, when refinancing makes sense.

- Second home or investor

- Focus: pricing differences, cash reserves, insurance and condo rules.

- Buying new construction

- Focus: rate locks, builder incentives, closing timeline.

What “mortgage rates under 6%” really means in Florida

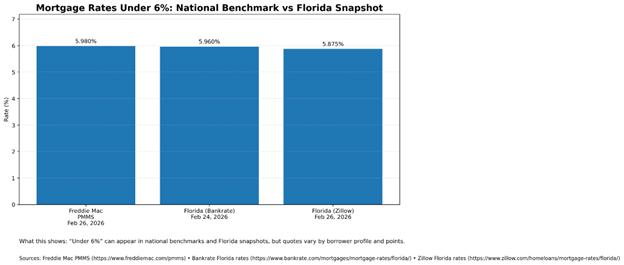

“Under 6%” usually refers to a benchmark, like the national weekly average for a 30-year fixed mortgage, not a promise you will personally get that rate.

For example, Freddie Mac’s Primary Mortgage Market Survey reported the average 30-year fixed rate at 5.98% as of February 26, 2026.

In Florida, you may also see sub-6% options during the same week, but your actual quote depends on factors like:

- credit score and debt-to-income ratio,

- down payment and loan size,

- points and lender fees,

- property type (condo versus single-family),

- occupancy (primary residence versus second home).

If you want a Florida-specific snapshot, large rate aggregators publish Florida rate tables that can land anywhere from the mid-5% to low-6% range depending on day and borrower assumptions.

Bottom line: “Under 6%” can show up in real quotes for well-qualified borrowers, but it is sensitive to credit, points, and loan type.

How much can under-6% rates change your buying power?

Even small rate moves can matter in monthly payment terms.

A practical way to use the “under 6%” window is not to chase the lowest number. Instead, set a payment target and stress test it.

Build your real monthly payment target

Include:

- principal and interest,

- property taxes (estimate),

- homeowners insurance (estimate),

- flood insurance (if applicable),

- HOA or condo fees.

Stress test your budget

Ask one question before you write an offer:

If the rate moves back above 6% before I lock, does this still work?

If the answer is no, the deal is fragile.

Florida housing trends: why rate dips can create negotiation openings

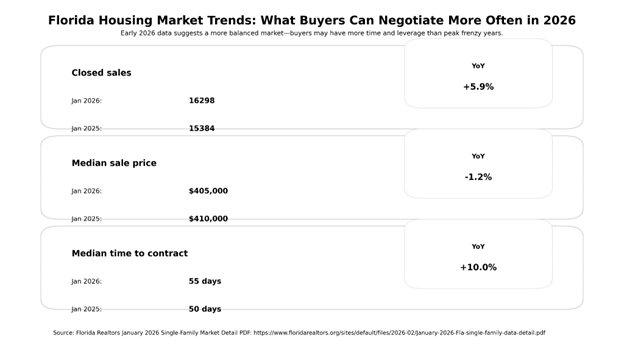

Rate dips often pull buyers off the sidelines. At the same time, Florida has shown signs of a more balanced tempo than the frenzy years.

In Florida Realtors’ January 2026 statewide single-family report:

- closed sales were up year over year,

- the median sale price was slightly down year over year,

- median time to contract increased to 55 days (up from 50 days).

That time-to-contract detail matters. More time can mean more choice and, in the right situations, more room to negotiate.

A Florida opportunity pattern worth watching

- resale listings that sat through the holidays may be more open to credits or price adjustments in Q1 and Q2,

- buyers who come prepared with financing and inspection strategy can use the softer tempo to negotiate repairs or seller-paid closing costs.

Where the best opportunities show up when mortgage rates dip

When mortgage rates fall, the obvious benefit is a lower payment. In Florida, quieter opportunities often come from how sellers respond.

1) Seller credits and buydowns

Instead of pushing price down, a seller may offer a credit that can help you:

- reduce closing costs,

- fund an allowed temporary buydown (program availability varies),

- pay for repairs or insurance-related updates.

2) Timing advantage for prepared buyers

When more buyers re-enter, the advantage shifts to people who already have:

- a clean pre-approval,

- documented funds,

- a clear “walk-away” payment number.

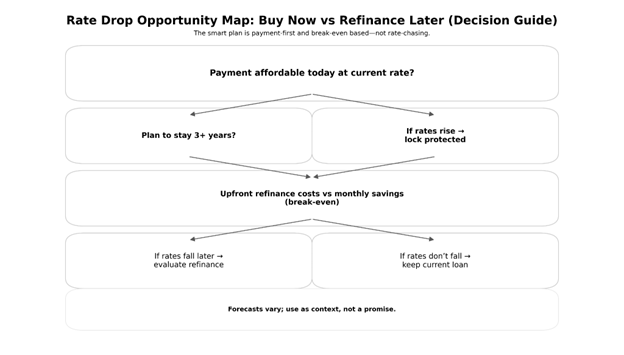

3) A refinance “second chance” plan

If you buy now and rates drop further later, refinancing may be an option.

That is not automatic. It depends on costs and your time horizon.

Refinance rates in Florida: when refinancing makes sense and when it does not

Refinancing can be powerful, but it is not “free money.” Use a break-even mindset.

Break-even checklist

- What are the total refinance costs (lender fees, title, escrow, and related costs)?

- How much do you save per month?

- How many months does it take to break even?

If you plan to move in two years, a refinance that takes 36 months to break even may not be worth it.

What forecasts can and cannot do

Market outlooks can help set expectations, but they are not guarantees. For example, Fannie Mae’s September 2025 outlook forecast rates ending 2026 around 5.9%, and the Mortgage Bankers Association publishes forecast tables tied to the Freddie Mac 30-year fixed series.

Takeaway: Many outlooks point to rates hovering around the 6% zone rather than collapsing dramatically lower.

Common mistakes Florida buyers make when rates fall

- shopping only the interest rate, not APR,

- paying points without a plan (points can be smart, but only if you keep the loan long enough),

- skipping insurance budgeting (get quotes early),

- not locking when the deal is affordable (trying to time the exact bottom can backfire),

- overbidding because “rates are better,”

- ignoring condo rules and reserves if buying a condo (guidelines can be stricter).

Step-by-step roadmap for Florida home buying in 2026

1) Define your payment comfort zone

Mini-checklist:

- max monthly payment you can afford comfortably,

- emergency buffer for insurance and tax increases,

- HOA or condo fee tolerance.

2) Get a pre-approval that matches your real plan

Confirm:

- loan type,

- down payment,

- estimated cash to close,

- what a credit or score change could do to pricing.

3) Watch rates, but do not chase them daily

Track a public benchmark weekly, then focus on your lender quote and lock strategy.

4) Write offers with negotiation leverage

- consider seller credits to offset closing costs,

- keep inspection and insurance timelines realistic.

5) Lock your rate when the numbers work

- confirm the lock period fits the closing timeline,

- review points and fees carefully.

6) Close with a first-year plan

- keep a homeownership budget,

- set reminders for insurance renewals and escrow reviews.

The Bridge: why professional help matters

A rate headline is not a strategy.

A mortgage professional can help you:

- compare lender pricing (rate, points, and APR),

- choose a lock strategy that matches your closing timeline,

- evaluate seller credits versus price reductions,

- budget Florida-specific costs like insurance, HOA, and flood exposure,

- build a buy now versus refinance later plan that actually pencils out.

Optional mini case study (anonymous)

A buyer found a home that looked affordable with a sub-6% quote, but the initial insurance estimate was far too low.

After getting real insurance quotes early, they adjusted the target price range and negotiated a seller credit to offset upfront costs. The result was a monthly payment that still worked even after escrow changes.

FAQ

Are 30-year mortgage rates in Florida really under 6%?

Some borrowers have seen sub-6% Florida quotes in late February 2026 depending on profile and points, while a national benchmark also dipped under 6%. Your actual rate depends on credit, down payment, loan type, and lender pricing.

What is the most reliable benchmark for mortgage rates?

Freddie Mac’s Primary Mortgage Market Survey is a widely cited weekly benchmark for 30-year fixed rates.

Should Florida buyers wait for even lower rates?

Trying to time rates perfectly is risky. A better approach is buying when the payment works and the home fits your goals, then refinancing later if it truly saves money.

What matters more than the rate in Florida?

Insurance, taxes, HOA fees, and property condition can swing monthly costs significantly. Many buyers regret not pricing these in early.

Do lower rates mean Florida home prices will jump?

Lower rates can increase demand, but local inventory, affordability, and seller behavior also matter. January 2026 Florida data also showed a longer time to contract and a slightly lower median single-family price year over year.

Is refinancing always worth it if rates drop?

Not always. Compare total costs to monthly savings and calculate a break-even timeline.

How do I use seller credits when rates are near 6%?

Seller credits can help cover closing costs or support certain buydown structures (availability varies). The best use depends on how long you expect to keep the mortgage.

What should a first-time Florida buyer do first?

Get a pre-approval, estimate full monthly costs (insurance plus taxes plus HOA), and define a payment limit before you fall in love with a listing.

Wrap-up

Mortgage rates under 6% can create real opportunities for Florida buyers, but the best wins usually go to buyers who stay disciplined.

- Budget the full monthly cost.

- Use negotiation tools like seller credits.

- Lock a deal when the payment fits your life, not when the internet says the rate is perfect.

If you want help comparing current Florida mortgage rates, choosing a lock strategy, or building a buy versus refinance plan for Florida home buying in 2026, speak with a mortgage professional.

Sources & References

Freddie Mac — Primary Mortgage Market Survey (PMMS), weekly 30-year fixed averages:

https://www.freddiemac.com/pmms

FRED (St. Louis Fed) — 30-Year Fixed Rate Mortgage Average in the United States (MORTGAGE30US):

https://fred.stlouisfed.org/series/MORTGAGE30US

Bankrate — Florida mortgage rates (state snapshot tables):

https://www.bankrate.com/mortgages/mortgage-rates/florida/

Zillow — Florida mortgage rates (state snapshot):

https://www.zillow.com/homeloans/mortgage-rates/florida/

Florida Realtors — January 2026 Single-Family Market Detail PDF:

https://www.floridarealtors.org/sites/default/files/2026-02/January-2026-Fla-single-family-data-detail.pdf

Fannie Mae — Mortgage rates expected to move below 6% by end of 2026 (Sept 2025 outlook summary):

https://www.fanniemae.com/newsroom/fannie-mae-news/mortgage-rates-expected-move-below-6-percent-end-2026

Mortgage Bankers Association — Mortgage Finance Forecast (Jan 2026 PDF):

https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/2026/mortgage-finance-forecast-jan-2026.pdf