If you’ve looked at your escrow statement lately and thought, “Why did my payment jump again?”, you’re not imagining it. In Florida, property taxes can change your monthly mortgage payment even if your interest rate never moves.

And in Florida property tax reform 2026, the conversation is louder than it’s been in years. Several proposals aim to reduce, or eventually eliminate, certain parts of property tax bills for homestead homeowners.

That sounds like great news. It can also get confusing fast. This guide breaks the situation down in plain English and gives you a practical plan you can use now—whether you already own a home, you’re buying in 2026, or you’re simply trying to understand what could change.

Quick start: pick your path

Use this checklist to jump straight to what matters most.

If you own a home and your payment is escrowed

- Pull your most recent escrow analysis from your lender.

- Find your TRIM notice (more on TRIM below) and keep it in your records folder.

- Confirm you’re receiving every exemption you qualify for—especially homestead.

- Build a “property tax buffer” into your budget for 2026–2027 (escrow changes can lag).

If you’re buying a home in Florida in 2026

- Ask your lender for two estimates:

- an “expected” escrow estimate, and

- a more conservative “stress‑tested” estimate.

- Learn how homestead eligibility timing can affect your first year of taxes.

If you think your assessed value is too high

- Start with your county property appraiser (often the fastest way to clarify what changed).

- Note your appeal window—deadlines are typically tied to the TRIM notice mailing.

If you keep hearing “property tax cuts Florida ballot”

- Focus on what’s actually filed and moving through the Legislature.

- Watch for final ballot language and official effective dates.

- Don’t count savings until something is approved and implemented.

Florida property taxes in plain English

Florida property taxes are ad valorem taxes, meaning they’re based on value. Here’s the simplified flow:

- Just value: what the property appraiser estimates your home is worth.

- Assessed value: your value after assessment limits (for eligible properties).

- Taxable value: assessed value minus exemptions (like the homestead exemption).

- Millage rate: the “tax rate” set by local taxing authorities (county, city, school board, special districts).

- Tax bill: taxable value × millage, plus any non‑ad valorem assessments (separate line items).

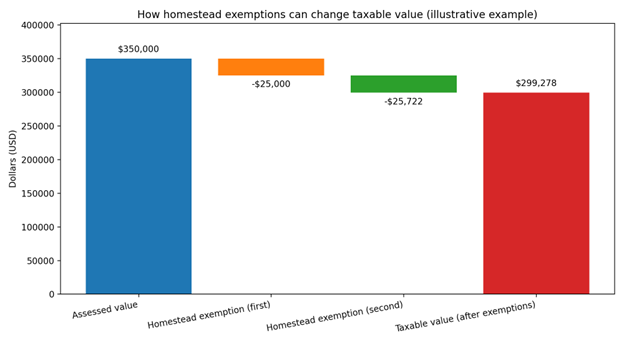

A Florida‑specific detail: homestead exemptions

Florida’s homestead exemption structure is layered. In general:

- The first portion can apply broadly.

- A second portion generally does not apply to school district taxes.

If that sounded like a lot, here’s the takeaway:

Your tax bill isn’t one tax. It’s a bundle of taxes from multiple entities—and many reforms target only certain parts of that bundle.

Why Florida property tax reform 2026 is a headline

A phrase you’ll see repeatedly in proposals and media coverage is:

“Non‑school property taxes”

This generally means everything except the school district levy—so county, city, and many special district taxes (depending on where you live).

That distinction matters because several proposals are written to:

- keep school taxes in place, while

- changing exemptions for non‑school taxes.

And because these proposals are framed as constitutional amendments, they typically involve:

- high vote thresholds in the Legislature to place on a ballot, and

- 60% voter approval to take effect.

Bottom line: When you hear “property tax relief,” translate it as possible future relief with timelines, conditions, and eligibility rules.

What’s being proposed for the 2026 cycle (high level)

Below are examples of major proposals discussed during the 2026 session that relate to homestead and non‑school property tax changes. These are high‑level summaries—always read the latest official text before acting.

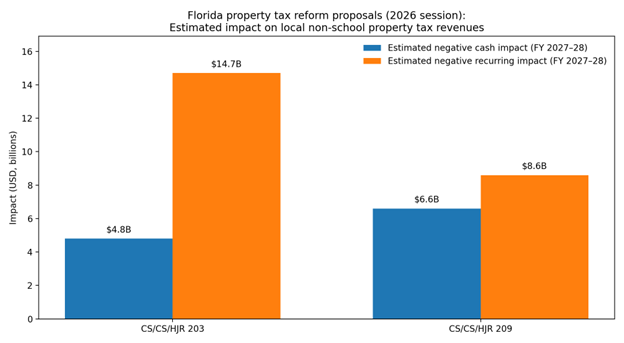

Proposal 1: A phased approach to eliminating non‑school property taxes for homesteads

One proposal, CS/CS/HJR 203, would increase the homestead exemption for non‑school taxes each year over a multi‑year phase‑in, with language that ultimately aims at a full exemption from non‑school ad valorem taxes in a specified year—while still excluding school taxes.

The proposal also includes provisions intended to limit how local governments reduce funding for certain first responder services below a defined base.

Practical implication: If you’re planning your budget, treat any savings as potential until there’s a finalized ballot measure, voter approval, and a confirmed effective date.

Proposal 2: A larger “insurance‑linked” alternative exemption

Another proposal, CS/HJR 209, would create an alternative second homestead exemption for homestead properties that meet an insurance requirement. The concept is a much larger exemption for non‑school taxes for insured homestead owners.

This proposal also includes a first‑responder funding provision and specifies an effective date after voter approval.

Decision checkpoint: If your homeowners insurance situation is complicated (coverage gaps, recent non‑renewals, or changing carriers), don’t assume you’ll qualify for an insurance‑linked exemption without checking the final eligibility language.

What this could mean for your monthly mortgage payment

If you escrow, your lender collects property taxes monthly and pays the bill when due. If expected taxes drop, your payment may drop later—but it’s rarely instant.

Here’s why:

- Escrow payments are based on estimates and recalculated on a schedule.

- Tax changes may show up only after the next assessment/tax cycle reflects them.

- Lenders often keep an escrow cushion to reduce the risk of shortages.

This is also why many homeowners feel “payment shock” without a rate change: property taxes and insurance can move faster than your budget.

If reform passes, you might see:

- a lower tax line item in the future,

- a revised escrow payment after your lender’s next analysis, and

- a possible refund/overage later (depending on how escrow was collected).

You could also see:

- a lag of months before savings show up,

- different results by county/city based on millage and local budget responses.

A step‑by‑step roadmap to prepare (no matter what happens)

This is the “do this now” plan you can follow even if nothing changes.

1) Gather your key documents

- Most recent property tax bill

- Your TRIM notice (Notice of Proposed Property Taxes)

- Mortgage escrow analysis (if you have one)

- Proof of any exemptions you believe you qualify for

2) Confirm your homestead status and exemptions

In Florida, homestead exemption applications generally run through your county property appraiser. If you bought recently, double‑check you didn’t miss a deadline or a documentation step.

Net‑net: Before you worry about new reforms, make sure you’re getting the benefits available under current law.

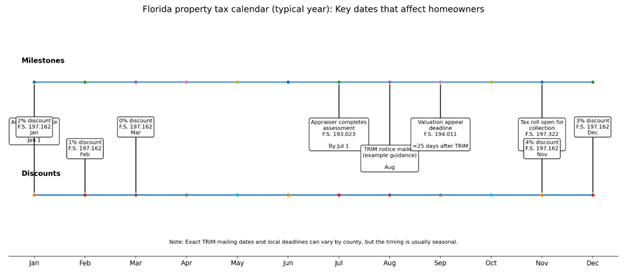

3) Learn the annual property tax calendar (so deadlines don’t sneak up)

A few anchor points are consistent year to year:

- Property is assessed as of January 1.

- Property appraisers generally complete assessments by July 1 (with limited extension options).

- TRIM notices are typically mailed in August (timing varies by county).

- If you’re appealing valuation, petitions are generally due by the 25th day following the mailing of the TRIM notice.

- Tax collection typically opens around November 1, with early‑payment discounts offered by statute.

4) Stress‑test your budget (especially if you plan to buy)

Ask for two numbers from your lender or mortgage professional:

- your “expected” escrow estimate, and

- a more conservative estimate assuming taxes/insurance are higher than expected.

This helps you plan for 2026 without panic.

5) Track reform updates the smart way

Instead of relying on social media summaries:

- Track official bill pages and staff analyses.

- Watch for ballot placement and confirmed effective dates.

- Remember: constitutional amendments usually require 60% voter approval.

Common mistakes homeowners make during property tax changes

- Assuming reform guarantees a lower bill. Many proposals depend on elections, timelines, and eligibility details.

- Confusing assessed value with taxable value. Your bill is based on taxable value after exemptions.

- Missing the appeal deadline. The petition window can be short and is often tied to TRIM mailing.

- Forgetting escrow lag. Even when taxes change, escrow recalculations can trail behind.

- Assuming homestead is automatic. In most cases, you must apply through your county property appraiser.

“What this means for you” scenarios

If you’ve owned your home for years

You may already benefit from assessment limits and exemptions. Reforms targeting non‑school taxes could still matter, but your impact depends on your taxable value and your local millage.

If you bought recently

In many Florida markets, taxes can reset higher after a sale. Reforms might help later, but your immediate plan should assume current law until something is finalized.

If you’re buying in 2026

Your “all‑in” payment isn’t just the mortgage:

- mortgage principal + interest

- property taxes

- homeowners insurance

- HOA (if any)

So here’s the move: Build a buffer so your plan still works if taxes and insurance land higher than the first estimate.

FAQ

Is Florida eliminating property taxes in 2026?

As of February 18, 2026, the proposals actively moving are focused on reducing or phasing out non‑school property taxes for homesteads over time—not necessarily eliminating all property taxes statewide.

What does “non‑school” property tax mean?

It generally means property taxes that are not the school district levy—such as county, city, and some special district taxes.

Will my mortgage payment go down if taxes go down?

It may, especially if you escrow—but usually not immediately. Escrow updates can lag, and lenders may keep a cushion.

What is the TRIM notice and why should I read it?

TRIM stands for Truth in Millage. It’s designed to show which entities are taxing you and your proposed taxes, and it’s often tied to deadlines for challenges and hearings.

How long do I have to appeal my property value?

In many valuation cases, the petition deadline is on or before the 25th day following the TRIM notice mailing. Always confirm the exact deadline printed on your notice.

When are property taxes due in Florida?

Tax collection typically opens around November 1, with early‑payment discounts offered during the season.

Do I need 60% of voters for a property tax change to pass?

For constitutional amendments, Florida generally requires 60% voter approval.

I heard about “property tax cuts Florida ballot.” How do I know what’s real?

Look for official bill text and staff analyses on state legislative pages, plus ballot certification details from state election resources.

The Bridge: why professional help matters (especially with escrow)

Even if tax reform passes, the “real world” impact usually shows up through:

- lender escrow calculations,

- timing of assessment cycles,

- insurance and exemption paperwork, and

- closing‑year estimates for new buyers.

A generic online payment calculator usually can’t account for:

- when your homestead benefit starts,

- how escrow cushions affect your monthly payment,

- county‑specific timing, or

- how changes in taxes and insurance interact during underwriting.

If you’re buying, refinancing, or trying to avoid escrow surprises, a quick review can help you stress‑test your payment before you commit to a number that feels comfortable only on paper.

Conclusion: a friendly reminder before you plan your budget

Florida property tax reform 2026 is still a moving target. Credible headlines can skip key details like eligibility, local millage responses, and effective dates. Use what you’ve read here as a planning framework—not personal tax or legal advice.

Top takeaways:

- Property taxes are a bundle (county/city/school/special districts), and reforms may target only parts of it.

- Escrow changes lag—even real tax savings often show up months later.

- Your best move today is confirming exemptions, watching TRIM deadlines, and budgeting with a buffer.

If you’re buying or refinancing this year, consider a quick payment review with a mortgage professional so your plan still works under different tax scenarios.

Hard next step: Stop guessing. Book a 15‑minute payment review. Bring your current escrow analysis (or your purchase price and insurance quote) and we’ll walk through a conservative monthly payment range.

Schedule a mortgage payment review today.