If you own a home in Florida, you’ve probably had that moment: you open a renewal notice and think, “How is this even possible?” Or you worry your monthly payment could jump—even if your interest rate doesn’t—because your home insurance changed.

That tension is the “crossroads” Florida homeowners are heading into in 2026. There are real signs the market is shifting. But many households are still dealing with high premiums, stricter underwriting, and surprise costs that ripple into the mortgage.

This guide is here to help you understand what’s happening, what it could mean for your budget, and what to do next—without panic.

Disclaimer: This article is for educational purposes only and is not financial, legal, or tax advice. Insurance rules, underwriting, and lender requirements vary by insurer and borrower.

Quick help: Want to sanity-check how a renewal could affect your payment?

Quick start: pick your path

Choose the situation that fits you best:

- Renewal coming up → Focus on shopping, mitigation credits, and documentation.

- On Citizens → Understand the glidepath cap, depopulation offers, and your options.

- Buying in 2026 → Plan for the “all-in” payment so you don’t get blindsided at underwriting.

- Refinancing or using a HELOC → Know how insurance + escrow affects affordability and approval.

- Trying to remove PMI → Make sure insurance costs don’t erase the savings.

Mini checklist (10 minutes)

- ☐ Find your current policy’s annual premium and renewal date.

- ☐ Check your mortgage statement: is insurance escrowed (paid through the mortgage)?

- ☐ Ask your agent for your wind mitigation report and roof documentation (if available).

- ☐ Get at least two quotes (even if you don’t switch).

- ☐ Update your budget using a “high renewal” scenario.

Why 2026 feels like a crossroads in Florida

“Crossroads” doesn’t mean everything is suddenly fixed—or suddenly worse. It means the direction of travel is changing, and homeowners will experience that change at different speeds depending on county, roof condition, claims history, and carrier appetite.

The market has been under pressure for years

Florida’s regulators have repeatedly pointed to the frequency and severity of litigated claims as a major driver of instability, and the state has gone through multiple reform waves (2019–2023) intended to reduce litigation and improve market stability.

Citizens is shrinking—and that matters

Citizens is Florida’s insurer of last resort. When Citizens grows quickly, it often means the private market is tight. When Citizens shrinks, it can signal more private-market capacity—but it doesn’t guarantee lower premiums for everyone.

The key takeaway: you can see the market improving and still have a rough renewal, depending on where you live and how your home underwrites.

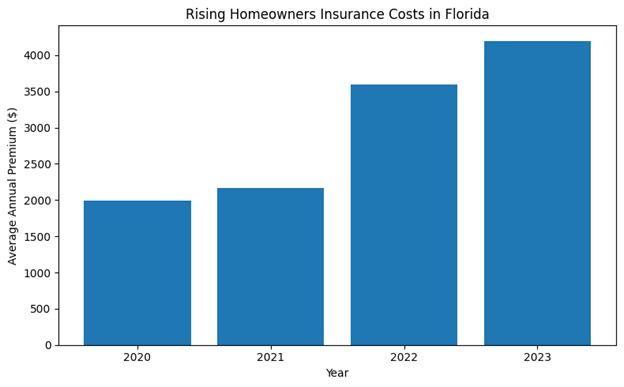

Premiums can vary wildly by county

Even within the same state, home insurance pricing can look completely different from county to county—especially when wind coverage is included.

For example, Florida’s Office of Insurance Regulation has shown county-level averages (as of March 31, 2025) ranging from roughly $2,084 in Sumter to $7,621 in Monroe for homeowners premiums including wind.

Chart 1: Average homeowners premium by county (including wind)

Bottom line: headlines are statewide, but your premium is local.

How this can hit your monthly payment

This is the part most homeowners feel immediately: the all-in monthly payment.

If your insurance is escrowed, your mortgage payment can change

Many homeowners pay insurance through an escrow account collected with the mortgage payment. When the premium changes, your servicer typically adjusts the escrow portion of your payment.

Here’s what that can mean:

- Higher premium → higher monthly payment.

- Escrow shortage risk. If your escrow account didn’t collect enough to cover the bill, you may need to “catch up.”

- Payment volatility. The change can land in one letter, even if nothing about your loan changed.

Decision checkpoint: If you’re escrowed, treat renewal season like a mini “re-qualification” of your budget.

If you’re buying in 2026, insurance can affect qualification

Most lenders qualify you based on the full housing payment—not just principal and interest. If your insurance estimate jumps, it can reduce the purchase price you feel comfortable with (or even what you qualify for), even if the rate is unchanged.

Practical tip: run two scenarios when you shop homes:

- A best-case quote

- A stress-test quote that’s meaningfully higher

If you’re refinancing, the math is more than the rate

A refinance can still be a smart move—but higher insurance (and taxes) can shrink the monthly savings. Make the decision based on the all-in payment, not the headline rate.

[Internal link: refinance break-even checklist]Chart 2: Example how a premium increase affects monthly cost

Citizens in 2026: glidepath capping, rate proposals, and what to watch

If you’re on Citizens, 2026 has a few moving parts worth understanding in plain English.

The glidepath cap is moving to 15%

Citizens explains that annual rate changes are subject to “glidepath” capping. For many primary personal-lines policies, the cap is set to 15% effective January 1, 2026 (with exclusions such as coverage changes and certain adjustments).

Translation: even if the “indicated” change would be higher, the cap may limit year-over-year increases for many policyholders. But the details depend on your policy type and situation.

Citizens has discussed rate decreases for many policyholders

Citizens’ Board approved 2026 rate recommendations that include:

- A 6% statewide average decrease for personal lines

- About three out of five policyholders receiving an average reduction (reported as 5%)

- A potential effective date of June 1, 2026, following regulatory review

Important: these are recommendations subject to the regulatory process, and results vary by policy.

Chart 3: Changes in Monthly Payment in Escrow with and without Insurance

The moves that actually help: how to protect your budget in 2026

You can’t control hurricane seasons—or the entire market. But you can control how prepared you are.

Focus on the levers that most often move the needle

- Documentation: roof age, permits, mitigation features, inspection reports

- Shopping: even if you like your current carrier, quotes give you leverage and clarity

- Deductibles: know what you agreed to before storm season

- Budget buffer: plan for renewal volatility—especially in higher-cost counties

Use programs designed to improve resilience

Florida’s My Safe Florida Home program offers free wind-mitigation inspections and grant assistance for eligible homeowners to strengthen homes against hurricanes.

Even if you don’t receive grant funding, the inspection and documented mitigation features can help when shopping coverage.

Common mistakes homeowners make right now

- Waiting until the last minute to shop (less time = fewer options)

- Assuming escrow will “smooth it out” (it can still raise your payment and create shortages)

- Dropping coverage without understanding lender requirements (many mortgages require hazard insurance)

- Not documenting upgrades (a better roof doesn’t help your quote if no one can verify it)

- Over-focusing on statewide headlines instead of your county’s reality

- Treating Citizens as “set it and forget it” (offers and market shifts can change your options)

Step-by-step roadmap for homeowners in 2026

1) Gather the right documents first

- Declarations page (current policy)

- Renewal offer (if available)

- Wind mitigation report (if you have one)

- Roof info: age, permits, receipts, photos (if available)

- Mortgage statement showing escrow (if escrowed)

2) Confirm your real housing cost

Build a simple monthly estimate:

- Mortgage principal + interest

- Property taxes

- Home insurance

- Flood insurance (if needed)

- HOA/condo dues

3) Shop strategically

- Get quotes that match your current coverage apples-to-apples

- Ask what changes meaningfully reduce premium (deductible, documentation, mitigation)

- If you’re on Citizens, understand the timing and rules around offers and renewals

4) Plan for escrow movement

If your premium increases, be ready for:

- Higher monthly escrow

- Possible shortage repayment

5) If you’re buying, do insurance due diligence early

Before you fall in love with a home:

- Ask for roof details and any claims history you can access

- Get an insurance quote while you’re under contract (timing matters)

- Keep a budget cushion for renewal volatility

The bridge: why professional help matters

Online advice can get you 80% of the way there. The tricky part is the last 20%—the part that depends on your timing, escrow setup, and lender requirements.

A mortgage professional can help you:

- Model a conservative all-in payment (including insurance + escrow adjustments)

- Stress-test affordability before you commit to a purchase, refinance, or HELOC

- Compare options across multiple lenders, not just one institution

Example scenario (realistic, not a promise)

A homeowner sees a renewal increase and assumes escrow will “handle it.” Their payment jumps, and the lender also bills an escrow shortage. With a quick payment review, they plan a buffer, shop coverage earlier, and avoid a last-minute scramble.

FAQ

Is Florida home insurance actually getting better in 2026?

There are signs of stabilization and Citizens has discussed rate recommendations that include average decreases for many personal-lines policyholders. But outcomes still vary widely by county, property type, and insurer.

Why is my friend’s premium so different from mine?

Location matters, but so do roof age, mitigation features, rebuilding costs, proximity to the coast, and claims history.

What is the “glidepath” on Citizens?

Citizens describes glidepath capping as a limit on annual rate changes, with the cap moving to 15% effective January 1, 2026 (subject to exclusions and policy specifics).

Can my mortgage payment go up even if my interest rate doesn’t?

Yes. If insurance is paid through escrow, higher premiums can raise your monthly payment and may create escrow shortages.

Should I switch insurers just to get a lower price?

Price matters, but so do deductibles, exclusions, claim service, and coverage details. Compare quotes—but make sure it’s apples-to-apples.

What can I do that may actually lower my premium?

Wind mitigation documentation and certain upgrades can help some homeowners. My Safe Florida Home inspections (and eligible upgrades) may help when shopping.

If Citizens is lowering rates, will mine definitely go down?

Not necessarily. Recommendations describe averages and portions of policyholders; individual results vary and depend on regulatory approval and your policy details.

I’m buying in 2026—what’s the single biggest insurance mistake to avoid?

Underestimating insurance until the end. Get an early quote so your budget is based on the all-in payment, not a guess.

Conclusion: your 2026 action plan

Three takeaways to keep you steady:

- Treat renewal season like a budget event. If you’re escrowed, your payment can change quickly.

- Documentation + shopping are your best tools. Don’t wait until the last minute.

- Plan with the all-in payment. Rates matter, but so do insurance and taxes.

If you want help planning around insurance costs—especially how they affect your monthly payment, approval, or refinance options—we can run the numbers and map out a conservative plan for 2026.

Ready for a payment stress test?