Estimated Read Time: ~8 minutes

Last Updated: February 2026

Picture this: you finally get the keys. The excitement is real—until the first full month hits. The mortgage drafts. Escrow is higher than expected. HOA fees show up. Suddenly, the money you used to enjoy is gone.

You’re not broke on paper. You’re house poor.

If that’s one of your biggest fears as a first-time buyer, that’s not overthinking—it’s good judgment.

The good news? Becoming house poor is largely avoidable when you plan around the real cost of owning a home—especially in Florida, where insurance, taxes, and HOA fees can be decisive. This guide walks through how to set a safe price range, protect your savings, and buy with confidence.

Important: This article is for educational purposes only. It is not financial, legal, or tax advice. Costs and rules vary by lender, county, and personal circumstances.

Quick Start: Pick Your Path

If you only do one thing from this article, do this: base every decision on your all-in monthly payment.

Choose where you are right now:

- Not shopping yet: Build your all-in monthly number and set a hard ceiling.

- Getting pre-approved: Confirm taxes, insurance, HOA, and buffers are included.

- Touring homes: Re-check affordability using total payment—not list price.

- Under contract: Stress-test the payment using your Loan Estimate and insurance quotes.

- Closing soon: Protect your emergency fund and plan for year-one surprises.

Mini Checklist (Save This)

- ☐ Calculate your all-in monthly payment (not just principal + interest)

- ☐ Budget closing costs (often ~2–5% of purchase price, separate from down payment)

- ☐ Keep a meaningful cash buffer after closing

- ☐ Confirm taxes, insurance, and HOA before committing to a neighborhood

- ☐ Understand how mortgage insurance works—and how it can end

- ☐ Build a first-year house fund for repairs, escrow changes, and moving costs

What “House Poor” Really Means

Being house poor doesn’t usually mean missing payments. It looks more like this:

- Little room for groceries, gas, or childcare increases

- Car repairs turn into credit card balances

- Saving stops—or reverses

- Vacations and weekends quietly disappear

You can pay the mortgage, but you can’t breathe.

This happens when buyers anchor on the purchase price and underestimate the full monthly cost of ownership.

Plain English: An affordable home payment leaves room for life.

Build Your All-In Monthly Number (The One That Actually Protects You)

Most first-time buyers start with principal and interest. That’s only part of the picture.

A realistic monthly housing cost often includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- Flood insurance (when applicable)

- HOA or condo dues

- Mortgage insurance (PMI or FHA MIP)

- Ongoing maintenance and repairs

A Simple Way to Set a Safe Maximum

- Look at your monthly take-home pay.

- Subtract:

- Non-housing debts (car loans, student loans, credit cards)

- Essentials (food, utilities, healthcare)

- Savings goals (emergency fund, retirement, future plans)

- What remains is your comfortable housing range.

If a payment forces you to pause saving or rely on credit cards “temporarily,” that’s a warning sign.

Florida Reality Check: Costs That Commonly Surprise Buyers

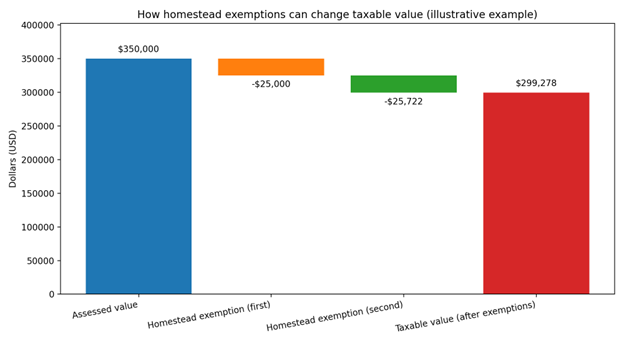

Property Taxes and the Homestead Exemption

Florida homeowners may qualify for a homestead exemption that can reduce taxable value and lower property taxes.

Two critical points:

- The exemption typically requires an application through your county property appraiser.

- Taxes can increase after purchase if the assessed value resets closer to market value.

Flood Insurance

Some properties require flood insurance based on flood zone and loan type. Even when not required, many buyers price it out anyway—especially in coastal or low-lying areas.

HOA and Condo Fees

A home that looks affordable on paper can become expensive fast with HOA dues. Treat HOA fees as a long-term fixed bill, not a minor add-on.

Fig 1: Monthly Payment With vs. Without HOA

Approved Is Not the Same as Affordable

Lenders rely on debt-to-income ratios to evaluate risk. That matters—but it doesn’t define your comfort level.

Your personal ceiling may need to be lower if:

- Your income varies

- Childcare costs are rising

- You support family members

- You’re planning major life changes

Bottom line: Your budget—not your pre-approval letter—should set the limit.

The Upfront Money Trap

A common path to being house poor looks like this:

- Stretch to buy the home you love

- Use savings for down payment

- Pay closing costs

- Furnish the home

- Move in with almost no cash left

Closing costs alone often fall in the 2–5% range of the purchase price, and moving costs add more.

Rule to remember: Never let the closing table wipe out your safety net.

Fig 2: Cash Needed Beyond Down Payment

Smart Strategies to Avoid Being House Poor

Treat Your Budget Like a Boundary

Choose a payment where you can still:

- Save every month

- Handle surprises

- Enjoy your life

Then shop within that number—not the lender’s maximum.

Compare Loans by Total Payment

Down payment size matters, but monthly impact matters more. Different loan programs affect insurance, fees, and long-term flexibility.

Understand Mortgage Insurance—and the Exit Plan

Mortgage insurance can be temporary on many conventional loans. Know when and how it could end so you’re not guessing.

Get Insurance Quotes Early

In Florida, insurance can swing affordability. Price it before you fall in love with a home.

Keep a “Life Happens” Buffer

Aim to keep:

- An emergency fund

- A starter home fund for early repairs and surprises

Even a modest buffer prevents stress-driven decisions.

Fig 3: Recommended Cash Buffers

Common Mistakes First-Time Buyers Make

- Shopping by list price instead of monthly payment

- Ignoring taxes, insurance, and HOA until late

- Draining savings for the down payment

- Assuming escrow never changes

- Falling in love with the max approval

- Skimming the Loan Estimate instead of studying it

A Step-by-Step Roadmap

- Define your real budget and minimum cash reserve

- Estimate an all-in payment using realistic assumptions

- Stress-test the numbers for future increases

- Get pre-approved with accurate neighborhood data

- Shop with guardrails—payment ceiling and must-haves

- Confirm the full cost before writing an offer

- Review the Loan Estimate carefully

- Close without draining your future

- Plan for the first year of ownership

Frequently Asked Questions

What does “house poor” mean in real life?

It means housing costs crowd out saving, flexibility, and enjoyment—even if bills are paid on time.

How do I know what I can really afford?

Build your budget from take-home pay and include taxes, insurance, and HOA—not just the mortgage.

Are closing costs part of my down payment?

No. They are separate and can be significant.

Why can payments rise after closing?

Changes in property taxes or insurance often affect escrow.

Is PMI permanent?

Often no, for conventional loans—under certain conditions.

Is an HOA always bad?

Not necessarily. The key is knowing what it covers and treating it as a fixed cost.

Final Thought

Buying your first home should increase your stability—not limit it.

If you’re purchasing in Florida and want help modeling payments, comparing options, and building a plan that protects your lifestyle, a personalized review can make the difference between stretching uncomfortably and buying with confidence.