If you are trying to build a home in Florida, buying the lot can feel like the “easy first step.” Then you talk to lenders and realize vacant land is not treated like a normal home purchase. Rates, down payment expectations, and approval rules can look very different, especially for raw land, rural lots, or properties that need utilities.

That is why many buyers search FHA Loan. An FHA Loan is known for flexible down payment rules, so it is natural to ask a simple question: Can an FHA Loan help me buy land and build a home in Florida?

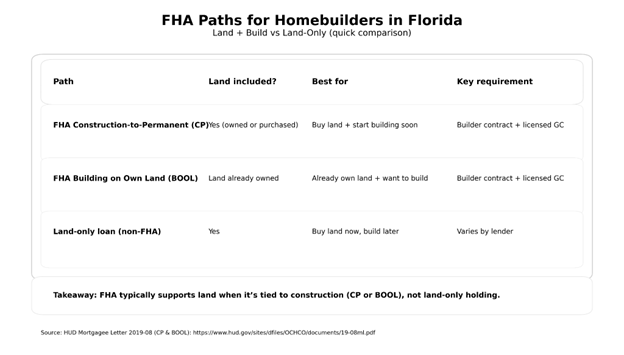

Here is the key: FHA financing is generally designed to insure mortgages on homes. It can support land when the land is part of an immediate construction plan, not a “buy land now, build someday” land-only loan.

Quick start: pick your path

- I want to buy land now and build later

- Focus: what FHA can and cannot do, and alternatives to FHA for land-only.

- I want to buy land and start building soon

- Focus: FHA construction to permanent, FHA one-time close loans, and a practical roadmap.

- I already own land and want to build a home in Florida

- Focus: Building on Own Land (often shortened to BOOL) and next steps.

- I am a Florida first-time home buyer loan shopper

- Focus: realistic cash requirements, builder requirements, and common mistakes.

- I keep hearing “FHA one-time close loan”

- Focus: the one-close flow, draws, inspections, and how land is handled.

What people mean by “FHA Loan land loan Florida”

Most consumers use “land loan” as a catch-all for any financing that helps them secure a lot.

Lenders usually mean one of these:

- Land-only loan (vacant land loan): financing for the lot only, with no immediate construction.

- Construction-to-permanent loan: one loan that funds construction and then becomes the long-term mortgage.

- Building on Own Land (BOOL): you already own the land and finance the permanent mortgage for the newly built home (and in some structures, pay off construction costs).

Bold key takeaway: An FHA Loan can sometimes include the land, but usually only when the land is tied to building a primary residence on a defined timeline.

Can an FHA Loan be used for a land-only purchase in Florida?

In most real-world cases, an FHA Loan is not used for a land-only purchase when there is no construction contract and no near-term build plan.

If your plan is “buy land now, build much later,” you usually need a different tool, such as:

- a land-only loan from a local bank or credit union,

- a private lender option (often with higher rates and down payment),

- cash, or

- a short-term structure that you refinance later (riskier and lender-specific).

If your plan is “buy land and build,” an FHA Loan may fit, if the lender offers the program and your file meets guideline requirements.

Decision checkpoint: If you do not have a builder and build plan, treat FHA as a long shot for land-only. If you are ready to build soon, keep reading.

FHA construction loan options in Florida that actually fit homebuilders

Most homebuilders who say “FHA land loan” are really looking for one of these two pathways.

1) FHA construction to permanent (often called an FHA one-time close loan)

This structure is often described as “one close” because there is typically one closing before construction begins.

In practical terms, it can include:

- land purchase (if you do not already own the lot),

- construction costs,

- and conversion to the permanent FHA mortgage after the build.

2) FHA Building on Own Land (BOOL)

If you already own the lot, this structure is designed for permanent financing of a newly built home on land you own.

In some setups, it can include paying off construction-related financing, depending on how the project is structured and what the lender allows.

Important reality check: Not every lender offers every FHA construction option. Availability is often lender-driven even when FHA rules allow a structure.

Bold key takeaway: When people want an “FHA Loan for land in Florida,” the workable answer is usually construction-to-permanent or Building on Own Land, not land-only.

Florida land is different: local issues lenders care about

Even if your income and credit are solid, Florida lots can trigger extra review.

Flood zones and flood insurance timing

If the future home will be in a Special Flood Hazard Area, federally backed loans typically require flood insurance once there is a building securing the loan.

What this changes for you:

- flood risk can affect approval conditions,

- insurance costs can change affordability,

- and some lots can be “technically buildable” but expensive to insure.

Permits and the Florida Building Code

Florida uses a statewide building code framework. Your builder and plans must meet local code and permitting requirements.

What this changes for you:

- lenders typically want confidence the home can be permitted,

- inspections and documentation must align with lender expectations,

- the certificate of occupancy is a common finish-line requirement.

The local-market factor many national guides miss

In many Florida counties, “buildable” is not just zoning. It is site readiness.

Lots that look affordable can become expensive when you add:

- clearing and grading,

- fill and drainage requirements,

- septic and well versus municipal hookups,

- stormwater rules.

Decision checkpoint: Before you buy a lot, get a rough site-work range. If the numbers are unclear, you are guessing with real money.

What builders and lenders typically require for FHA construction deals

What builders and lenders typically require for FHA construction deals

What builders and lenders typically require for FHA construction deals

What builders and lenders typically require for FHA construction dealsExpect the lender to ask for a real construction package, not just a lot address.

In plain English, you should be ready for:

- a signed construction contract,

- builder licensing and credentials,

- plans and specs,

- a detailed budget,

- a timeline and draw schedule (how funds are released during the build),

- inspections during construction.

Some FHA guidance and lender overlays emphasize that you must have a contracted builder, and the builder must be properly licensed. Lenders can also add stricter rules.

Bold key takeaway: Builder readiness is often the bottleneck, not borrower credit.

Common mistakes when trying to finance land plus build with an FHA Loan

- Buying the lot first without a construction financing plan.

- Assuming land-only financing and land-plus-build financing are the same.

- Choosing a builder who is not set up for lender documentation and draw schedules.

- Ignoring flood risk until late in the process.

- Underestimating site work (utilities, fill, drainage, permitting).

- Not budgeting for delays (permits, inspections, weather, storm season).

Step-by-step roadmap: from “lot found” to move-in day

1) Confirm your real goal

Ask:

- Do you want land-only (hold it) or land plus build soon?

- Do you have a builder picked, or only a lot?

2) Get pre-approved for the right product

Ask specifically about:

- FHA construction to permanent (one-time close),

- FHA Building on Own Land, if you already own the lot.

3) Validate the lot before you commit

Do these early:

- flood zone check (especially in coastal areas),

- access and utility feasibility,

- drainage and site-work expectations,

- permitting basics for the county and municipality.

4) Lock in your builder and contract

Your lender will usually want:

- a signed contract,

- specs and budget,

- proof of licensing and insurance,

- a draw schedule.

5) Finalize the full project budget

Include:

- land cost (if being purchased),

- construction costs,

- contingency,

- closing costs and reserves (lender-specific).

6) Close and start the build

With a one-close construction-to-permanent structure:

- construction begins after closing,

- draws and inspections happen during the build,

- conversion to the permanent mortgage happens after completion.

The Bridge: why professional help matters

Most online articles explain the concept. They do not help you win the edge cases.

A mortgage professional can help you avoid expensive mistakes, especially with:

- lender availability (many lenders simply do not offer these FHA structures),

- builder qualification and documentation,

- valuation and “as-completed” appraisal expectations,

- flood zone and insurance timing questions,

- lot readiness items that can derail budgets.

Value prop (plain language): We can help you compare lender options and program availability, so you are not building your plan around a loan that no one in your area will actually close.

FAQ

FAQ

FAQCan an FHA Loan finance buying land in Florida?

An FHA Loan can support land when the land purchase is tied to building a primary residence, such as through a construction-to-permanent structure.

Is there a true “FHA land-only loan” in Florida?

Most buyers asking this want land-only financing. FHA pathways generally focus on building a home, not holding vacant land indefinitely.

What is an FHA one-time close loan?

It is a common phrase for a construction-to-permanent setup where there is one closing before construction starts, then the loan becomes the permanent mortgage after completion.

Do I need a builder contract for FHA construction financing?

Usually yes. Expect to show a signed contract, plans, and a lender-acceptable builder.

What if I already own the land?

Building on Own Land is designed for constructing on land you already own, with permanent financing of the newly constructed dwelling.

Does flood zone status matter for construction loans in Florida?

Often yes. Flood insurance rules and mapping can affect planning, conditions, and insurance costs.

Does the Florida Building Code matter to lenders?

Yes. Permits, inspections, and code compliance are core to finishing the home and obtaining a certificate of occupancy.

What is the biggest budgeting surprise with buying land in Florida?

Site work. Clearing, fill, utilities, drainage, and permitting costs can be significant, and they vary widely by county and lot characteristics.

Conclusion and next steps

If you are searching “FHA Loan land loan Florida,” the clean way to think about it is land plus build, not land-only.

Top takeaways:

- An FHA Loan typically supports land only when it is part of a real construction plan.

- Builder readiness and documentation often decide whether the deal is financeable.

- In Florida, flood zones and site work can change the budget fast.

Stop guessing. Book a short build-financing review.

What happens next:

- We confirm your timeline (land-only vs land plus build soon).

- We identify which lenders in your area actually offer the right FHA construction structure.

- We map the documentation you will need so you can move faster once you find a lot.

Resources

- HUD FHA FAQ on minimum required investment (down payment concept): https://answers.hud.gov/FHA/s/article/What-is-the-minimum-down-payment-requirement-for-FHA

- FEMA flood risk and lending overview: https://www.fema.gov/flood-maps/know-your-risk/realtor-lending-insurance

- Florida Building Commission reference point: https://www.floridabuilding.org/c/default.aspx