Buying an investment property in Florida in 2026 starts with one rule: underwrite the real cost, not the story. A rental property may look attractive on a listing sheet, but the real decision depends on financing, insurance, flood exposure, taxes, reserves, and whether the property still works when your assumptions get more conservative.

Florida still attracts buyers because it offers a wide mix of markets, from urban condos to beach rentals to suburban single-family homes. But in 2026, buying an investment property is not as simple as finding a house and hoping rent covers the payment.

This guide explains how investment-property financing works in Florida, which costs matter most, how to choose a strategy, and what mistakes first-time and repeat investors should avoid before making an offer.

Want a fast first screen? Build the deal with realistic rent, real insurance quotes, vacancy, repairs, and reserve cash before you shop seriously.

Quick Start: Pick Your Path

- First-time investor: Focus on financing, reserves, and the mistakes section.

- Out-of-state buyer: Pay extra attention to insurance, flood zones, and local property management.

- High-budget buyer: Review conforming limits versus jumbo financing first.

- House hacker or small multi-unit buyer: Compare owner-occupied and investment-property rules carefully.

- Long-term rental buyer: Focus on cash flow, taxes, and local operating costs.

- Vacation-rental buyer: Verify local rules, insurance, and realistic occupancy assumptions before you buy.

What Counts as an Investment Property?

An investment property is a property you buy mainly to generate income or investment return rather than to occupy as your main home. In mortgage underwriting, that matters because lenders and loan investors treat occupancy type as a real risk factor.

Fannie Mae classifies loans by occupancy type, including principal residence, second home, and investment property. That is important because the loan terms, eligibility, and pricing conversation can change depending on how the property will actually be used.

That is why buyers should not confuse a second home with an investment property. If the real purpose is rental income or return, the financing path usually becomes stricter.

| Feature | Primary residence | Second home | Investment property |

| Main purpose | Owner lives there most of the time | Owner uses it personally part of the year | Income or investment return |

| Mortgage risk view | Usually lowest | Usually moderate | Usually highest |

| Underwriting | Often most favorable | Often stricter than primary | Often strictest |

| Income analysis | Based mainly on borrower income | Based mainly on borrower income | May include rental-income analysis |

| Best fit | Full-time housing | Personal getaway use | Long-term rental or return-focused strategy |

Key takeaway: Occupancy type is not a paperwork detail. It is one of the core facts a lender uses to price and underwrite the loan.

How Is Financing Different for an Investment Property in Florida?

Investment-property financing is usually stricter than owner-occupied financing. Lenders often look more closely at down payment, reserves, credit profile, existing debt, and whether the property still makes sense if rental income is uneven or delayed.

The first financing checkpoint in 2026 is loan size. If your loan amount rises above the applicable conforming limit, you may need jumbo financing. That often means a more document-heavy process and stronger reserve expectations.

For many buyers, that matters sooner than expected. Florida has a wide range of price points, and higher-cost homes can move into jumbo territory quickly.

Lenders may look closely at:

- Down payment size

- Verified income and assets

- Post-closing reserves

- Credit profile

- Property use

- Insurance affordability

- HOA dues, if applicable

A buyer should also budget beyond principal and interest. Taxes, insurance, and sometimes flood insurance can materially change the monthly payment.

Decision checkpoint: If the property only looks affordable before you add taxes, insurance, and reserves, the deal probably is not as strong as it first appears.

What Florida-Specific Costs Can Make or Break the Deal?

In Florida, the purchase price is only the start. Insurance, flood exposure, taxes, HOA dues, maintenance, and vacancy risk can change the economics of an investment property enough to turn a promising listing into a weak investment.

Flood risk is one of the biggest Florida-specific issues. Many investors make the mistake of checking flood exposure too late.

Insurance matters just as much. Premium differences can change cash flow materially from one property to another, even within the same metro area. Buyers should shop early and compare more than one quote.

Property taxes also deserve a close review. A buyer should not assume that tax treatment on a pure rental property will look like tax treatment on an owner-occupied Florida home.

Before making an offer, check:

- Flood-zone status

- Homeowners insurance quotes

- Wind and hurricane deductibles

- HOA fees and special assessments

- Property taxes and likely reassessment

- Ongoing maintenance needs

- Vacancy risk and turnover costs

Key takeaway: In Florida, the monthly carrying cost can drift far above the mortgage payment if you do not underwrite the property carefully.

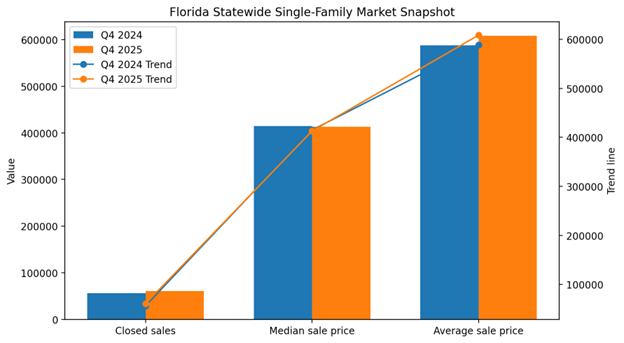

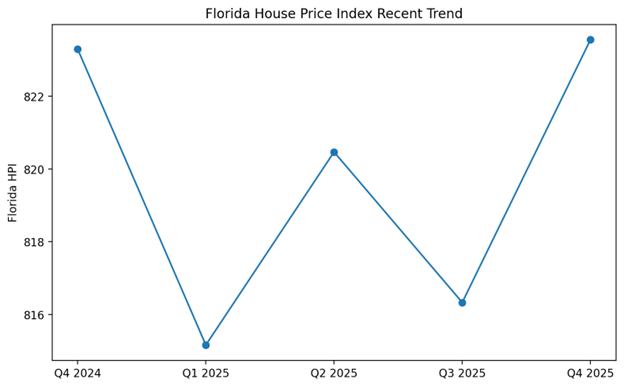

What Does Florida’s Market Look Like for Investment Buyers in 2026?

Florida’s market in 2026 looks more selective than the fastest post-pandemic years. Statewide activity is still strong, but the environment is less about panic buying and more about deal selection.

That can be good news for disciplined investors. More inventory and more measured price movement can create better due-diligence conditions than a market where every buyer is rushing.

That does not mean every local market is equally attractive. Florida is too large and too uneven for that kind of shortcut. Condo-heavy coastal markets, suburban rental corridors, and beach communities can all behave differently.

For investors, the practical takeaway is simple:

- Do not rely on statewide headlines as if they describe your property

- Watch local inventory, rent strength, and operating costs

- Focus more on cash flow and reserves than on automatic appreciation

Decision checkpoint: 2026 looks more like a selective-buying market than a “buy anything and wait” market.

How Should You Choose an Investment Property Strategy?

The right Florida investment property depends on your objective. A long-term rental, a small multi-unit property, and a vacation-rental-style property can each work, but they carry very different financing, management, vacancy, and rule-related risks.

For beginners, the safest first question is not, “Where will prices rise fastest?” It is, “What kind of risk can I actually manage?”

A practical way to think about it:

- Long-term rental: Usually steadier operating assumptions and simpler turnover patterns

- Small multi-unit property: Can spread vacancy risk across more than one unit, but may increase management and maintenance complexity

- Vacation-rental-style property: Can offer upside, but often brings more occupancy volatility, insurance complexity, local-rule sensitivity, and management effort

Rental tax treatment matters too. Rental income is generally taxable, and rental expenses may be deductible, but that does not make the property automatically profitable. You still need to underwrite the operating side honestly.

Key takeaway: The safest strategy is usually the one you can finance, manage, and hold through ordinary setbacks.

What Is the Step-by-Step Roadmap for Buying an Investment Property in Florida?

The practical path is to define your strategy first, qualify second, and analyze properties third. Buyers who reverse that order often fall in love with listings that do not fit their financing, risk tolerance, or actual goals.

Use this roadmap:

- Choose your strategy. Decide whether the property is for long-term rent, small multi-unit income, seasonal use, or a mixed personal-and-investment plan.

- Set a true budget. Include down payment, reserves, closing costs, taxes, insurance, HOA dues, and maintenance.

- Get pre-approved early. Ask how the lender will treat occupancy, reserves, and projected rental income.

- Check the loan size. If the amount may exceed the conforming limit, prepare for jumbo-loan underwriting.

- Screen for flood and insurance risk. Review flood-zone status and obtain real insurance quotes early.

- Underwrite conservatively. Use realistic rent assumptions, vacancy, repairs, and management costs.

- Review tax treatment. Understand how rental income and deductible expenses are generally reported.

- Make an offer with discipline. Do not waive critical protections just to win a deal faster.

- Re-test the deal before closing. Confirm final insurance, taxes, and payment figures still support the strategy.

Why Professional Help Matters

A mortgage calculator cannot tell you whether a property’s insurance bill will crush the cash flow, whether your occupancy plan changes the loan path, or whether the deal still works after reserves and vacancies are added.

That is where tailored guidance matters. A mortgage professional can help you:

- Compare primary, second-home, and investment-property financing paths

- Flag when jumbo financing may apply

- Review reserve and documentation expectations

- Pressure-test the monthly cost using real assumptions

At Pegasus, the goal is not just to get you pre-approved. It is to help you understand whether the deal is realistic before you commit.

Example Scenario

A buyer found a Florida property that looked attractive based on price and projected rent. But once flood risk, insurance quotes, HOA costs, and a realistic vacancy allowance were added, the numbers became much tighter. The better move was to adjust the target property type before making an offer, not after.

What Common Mistakes Do Florida Investment-Property Buyers Make?

Most bad investment property decisions come from optimistic assumptions, not a lack of listings.

Common mistakes include:

- Confusing a second home with an investment property

- Ignoring insurance until late

- Skipping flood-zone review

- Assuming owner tax benefits apply to rentals

- Underwriting with best-case rent

- Forgetting reserves and repairs

- Relying on statewide headlines instead of local market facts

Key takeaway: A weak deal usually reveals itself in the operating costs investors were hoping not to notice.

FAQ

Is buying an investment property in Florida still worth considering in 2026?

For some buyers, yes. Florida still offers active housing demand and diverse local markets, but 2026 looks more selective than the fastest-boom years. Buyers who focus on cash flow, insurance, and real carrying cost may find opportunities.

Do investment properties require bigger down payments?

Often, yes. Exact requirements vary by lender and loan structure, but investment properties are usually underwritten more conservatively than primary residences.

What loan limit matters in 2026?

The 2026 baseline conforming loan limit for one-unit properties in most areas is $832,750. Loans above the applicable limit may move into jumbo territory.

Does flood insurance matter for investment properties in Florida?

Yes. Flood risk can affect affordability, insurability, and resale even before it becomes a formal lender requirement.

Can I use homestead tax benefits on a rental property?

Usually not in the same way an owner-occupied permanent residence can. A pure investment property should not be underwritten as though it will receive homestead treatment.

How is rental income taxed?

Rental income is generally taxable, and rental expenses may be deductible. Reporting and tax treatment depend on the facts, so buyers should not guess.

Is a long-term rental safer than a vacation rental?

It may be, depending on your goals. A long-term rental often has steadier operating assumptions, while a vacation-rental-style property can involve more volatility and more management complexity.

Final Thoughts

The key insight is simple: buying an investment property in Florida in 2026 is less about chasing a hot market and more about buying with discipline.

- Check the financing path

- Check the insurance reality

- Check the flood exposure early

- Check the full monthly carrying cost

- Check whether the deal still works under ordinary conditions, not perfect ones

A Florida investment property may still be a smart move. It just needs to work as a real business decision after conservative assumptions, not before them.

If you want help sorting out financing options before you shop, speak with a mortgage professional early so you understand what you can realistically buy and how to structure the purchase more safely.

Sources & References

https://www.fhfa.gov/news/news-release/fhfa-announces-conforming-loan-limit-values-for-2026

https://www.fhfa.gov/news/news-release/fhfa-announces-conforming-loan-limit-values-for-2025

https://selling-guide.fanniemae.com/sel/b2-1.1-01/occupancy-types

https://singlefamily.fanniemae.com/media/26241/display

https://www.consumerfinance.gov/consumer-tools/mortgages/

https://www.fema.gov/flood-insurance

https://www.fema.gov/about/glossary/special-flood-hazard-area-sfha

https://agents.floodsmart.gov/resource-library/en/questions-answers-flood-insurance-real-estate-professionals

https://floir.gov/consumers

https://floir.gov/consumers/choices-rate-comparison-search

https://floridarevenue.com/property/Pages/Taxpayers_Exemptions.aspx

https://www.irs.gov/taxtopics/tc414

https://www.floridarealtors.org/sites/default/files/2026-01/4Q-2025-Fla-single-family-summary.pdf

https://www.floridarealtors.org/news-media/news-articles/2025/02/flas-jan-housing-new-listings-inventory-rise

https://fred.stlouisfed.org/series/FLSTHPI

https://www.fhfa.gov/reports/house-price-index/2025/Q4

https://fred.stlouisfed.org/series/ACTLISCOUFL