If your credit score is not perfect, applying for a HELOC can feel like walking into a test you did not study for. You may worry you will get declined, approved for a small line, or quoted a rate that makes the whole thing not worth it.

Here is the good news. A HELOC decision is rarely only about the score. Lenders are pricing risk, and risk is usually a mix of your home equity, your income stability, your monthly debt load, and your recent payment pattern.

Quick start: pick your path

- My score is below 680

- Go to: What lenders look for, Strengthen your application fast

- I have equity but high monthly debts

- Go to: How DTI affects approval

- I am self-employed or commission-based

- Go to: Documents that make underwriting easier

- I am worried about payment shock

- Go to: Draw and repayment periods

- I am married and the home is homestead

- Go to: Florida note on spouse signatures

What is a HELOC, and how does it work?

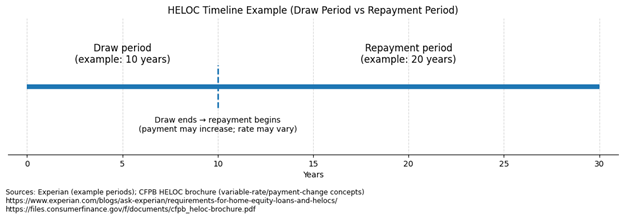

A HELOC (home equity line of credit) is an open-end line of credit secured by your home. You can borrow, repay, and borrow again up to your limit during the draw period. Many HELOCs have variable rates, so payments can change. After the draw period, you enter repayment, which can increase payments.

Key HELOC terms in plain English

- Home equity: your home’s value minus what you still owe on your mortgage.

- Draw period: the borrowing phase when you can access funds as needed.

- Repayment period: the phase after the draw ends, when the balance is repaid.

- Variable rate: the rate can change, which can change the payment.

CFPB explains that with variable-rate plans, payments may change even if you do not draw more money. CFPB also explains that repayment may be set over 10 or 15 years, or could involve a balloon payment depending on the plan.

Key takeaway: Before you apply, understand your payment in the repayment period, not just the payment during the draw period.

What lenders look for when your credit is not perfect

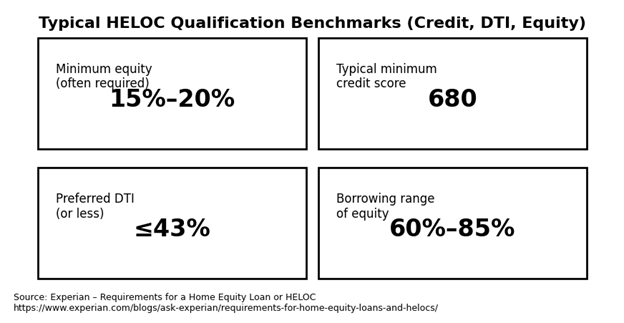

With imperfect credit, HELOC approval typically depends on your equity, your credit score, your recent payment history, your documented income, and your debt-to-income ratio (DTI). A common benchmark is at least 15 to 20 percent equity, a FICO score around 680, and DTI of 43 percent or less, but lender standards vary.

Typical benchmarks (use as a starting point, not a promise)

Experian summarizes common requirements lenders often use for a home equity loan or HELOC:

- Equity: often at least 15 to 20 percent.

- Credit score: many lenders look for FICO 680+, some want 720, and some may consider below 680 with strong equity or income.

- DTI: lenders typically prefer 43 percent or less.

- Borrowing range: many lenders allow borrowing around 60 to 85 percent of your home’s equity (varies).

Key takeaway: With imperfect credit, approval often comes down to whether the rest of your file looks clean and stable.

Key takeaway: With imperfect credit, approval often comes down to whether the rest of your file looks clean and stable.

How DTI affects HELOC approval, and how to fix it fast

DTI is your monthly debt payments divided by your gross monthly income. It matters because it shows whether you can handle another monthly obligation. Many lenders prefer DTI at 43 percent or less for home equity lending. If your DTI is high, paying down revolving debt is often the fastest fix.

A practical DTI improvement checklist

- Pay down credit cards first. This can improve both DTI and credit utilization.

- Avoid new loans before underwriting. A new car payment can change your file overnight.

- Document every income source you want counted (pay stubs, W-2s, tax returns, consistent deposits).

Decision checkpoint: If your DTI is high, prioritize lowering revolving balances before you shop HELOC offers.

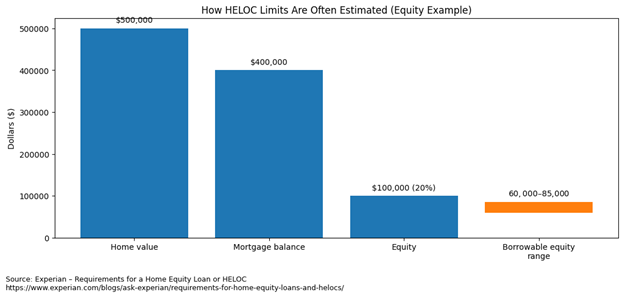

How much can you borrow with a HELOC?

Your HELOC limit is driven by your home value, current mortgage balance, and the lender’s combined loan-to-value limit. Lenders often cap how much they will lend against your equity, and an appraisal is commonly required to confirm value.

Experian gives a clear way to think about the math:

- If your home is worth $500,000 and you owe $400,000, your equity is $100,000 (20 percent).

- If a lender allows borrowing about 60 to 85 percent of that equity, the line might land roughly in the $60,000 to $85,000 range, depending on your full profile.

Key takeaway: More equity can sometimes offset a weaker score, but it rarely overrides unstable income or high DTI.

Key takeaway: More equity can sometimes offset a weaker score, but it rarely overrides unstable income or high DTI.

Draw period vs repayment period: avoid payment shock

Many HELOCs start with a draw period that can allow interest-only payments, then switch to a repayment period when principal and interest are due. When the draw ends, payments can jump. Some plans may require a balloon payment. Plan for the higher payment before you sign.

CFPB explains that some plans allow interest-only payments during the draw period and that payments may change with variable rates. CFPB also notes that repayment may be scheduled over 10 or 15 years, or could require paying the entire balance at once as a balloon payment, depending on the plan.

The Federal Reserve and other regulators have also warned about “payment shock” when HELOCs move from draw to repayment, especially where interest-only payments were allowed.

Decision checkpoint: If the repayment payment would strain your budget, consider a smaller line, a different product, or waiting until your finances improve.

Decision checkpoint: If the repayment payment would strain your budget, consider a smaller line, a different product, or waiting until your finances improve.

Florida-specific note: spouse signatures for a homestead HELOC

In Florida, the state constitution says that the owner of homestead real estate, “joined by the spouse if married,” may alienate the homestead by mortgage. In practice, many lenders and title companies require a spouse to sign certain HELOC documents even if the spouse is not on the loan.

This is not just a lender preference. It is tied to Florida’s homestead protections.

What to do next: If you are married, bring this up early so closing does not get delayed.

HELOC vs home equity loan vs cash-out refinance

A HELOC is a flexible line you borrow from as needed. A home equity loan is usually a lump sum with set payments. A cash-out refinance replaces your mortgage with a larger one. With imperfect credit, the right choice depends on DTI, equity, how long you need funds, and whether you can tolerate variable-rate risk.

| Feature | HELOC | Home equity loan | Cash-out refinance |

| How you receive funds | Borrow as needed | Lump sum | Lump sum via new mortgage |

| Rate type | Often variable | Often fixed | Fixed or adjustable |

| Best for | Ongoing needs | One-time project | Reworking the whole mortgage |

| Key risk | Rate changes, payment jump | Higher fixed payment | Closing costs, higher balance |

Key takeaway: Pick the structure that matches how you will use the money, not just the lowest advertised rate.

Step-by-step roadmap to improve HELOC approval with imperfect credit

The fastest path to better HELOC odds is improving the factors lenders rely on most: recent payment history, credit utilization, DTI, and documentation quality. Start by checking your credit report for errors, paying down revolving balances, organizing income paperwork, and shopping multiple lenders. Criteria vary, so comparisons matter.

Practical action sequence

- Pull your credit reports and dispute errors, especially incorrect late payments.

- Reduce credit card balances before you apply.

- Avoid opening new accounts right before underwriting.

- Build a clean income package.

- W-2 employees: pay stubs and W-2s.

- Self-employed: recent tax returns and clear business documentation.

- Confirm home value and mortgage balance.

- Expect an appraisal in many cases.

- Compare at least three offers.

CFPB encourages shopping and comparing HELOC offers so you can compare costs and features.

Common mistakes that cause HELOC denials

- Applying before paying down credit cards (DTI and utilization stay high).

- Taking on new debt right before underwriting.

- Submitting incomplete income documents (especially for self-employed borrowers).

- Ignoring the draw-to-repayment payment jump.

- Not reading fee terms (annual fees, early termination fees, appraisal fees).

- Not planning for Florida homestead spouse signature timing.

- Comparing only the rate, not the full HELOC terms.

The Bridge: why professional help matters

A HELOC is not just “a score and a rate.” It is underwriting.

What generic advice and online calculators often miss:

- lender-to-lender differences on minimum scores, max combined loan-to-value, and documentation standards,

- how to present self-employed income so it underwrites cleanly,

- whether points, fees, and rate structure actually make sense for your time horizon,

- Florida closing friction, including homestead spouse signatures.

Our value prop: We can help you compare options across multiple lenders, not just one institution, and package your file so it gets a fair read.

Optional case study (anonymous)

A Florida homeowner had strong equity but a score under 680 due to high credit card utilization. They were about to apply before paying down balances.

We helped them sequence the steps: pay down revolving debt first, document income clearly, then shop multiple lenders. The outcome was a stronger file and clearer terms, without relying on a single lender’s rules.

FAQ

Can I get a HELOC with a credit score below 680?

Sometimes. Many lenders look for around 680, but some may consider lower scores if equity and income are strong. The trade-off is often a smaller line or higher pricing. Shopping multiple lenders matters.

What credit score do you need for a HELOC?

There is no universal minimum, but many lenders commonly look for FICO 680 or higher. Some want 720. Some may go lower with strong compensating factors.

How much equity do I need for a HELOC?

A common benchmark is at least 15 to 20 percent equity. Lenders also cap how much they will lend against your equity.

What DTI do I need for a HELOC?

Many lenders prefer DTI at 43 percent or less, though standards vary.

Are HELOC rates fixed or variable?

Many HELOCs are variable-rate. CFPB notes your monthly payments may change even if you do not draw more money.

Does my spouse have to sign for a HELOC in Florida?

Often, yes, if the property is treated as homestead. Florida’s constitution includes language requiring the owner to be joined by a spouse if married to mortgage the homestead.

Conclusion and next steps

Top takeaways:

- A HELOC is not approved on score alone. Equity, DTI, and documentation drive the decision.

- Pay down revolving debt first if you can. It can help utilization and DTI at the same time.

- Plan for repayment payments, not just draw-period payments.

Stop guessing. Book a HELOC readiness review.

What happens next:

- We review equity, DTI, and your credit profile.

- We identify lenders whose HELOC guidelines fit your situation.

- We outline the exact documents to prepare so underwriting moves faster.

What to prepare:

- recent pay stubs and W-2s, or tax returns if self-employed,

- current mortgage statement,

- homeowners insurance declarations page,

- a quick list of monthly debts,

- the amount you want to access and the reason.

External sources (authority)

- Experian, HELOC requirements and common benchmarks

- CFPB, HELOC brochure (variable rates, draw period, repayment, balloon payment, shopping around)

- Federal Reserve, interagency guidance on end-of-draw payment shock

- Florida Senate, Florida Constitution Article X Section 4 (homestead, spouse joined to mortgage)