Buying a home in Florida used to be mostly about location, schools, and getting a fair deal. In 2026, many buyers are adding a new (and uncomfortable) question:

“Will this home still be affordable to keep—and insurable—five years from now?”

That anxiety isn’t dramatic. Climate Change is already influencing Florida real estate in practical, monthly-budget ways: more nuisance flooding, higher repair risk, bigger insurance bills, and tighter closing requirements in certain areas. The result is a market where two homes with the same square footage can have very different true cost of ownership.

This guide breaks down the hidden gaps behind Florida’s coastal property market, why flood zone homes are a different category of purchase, and what you can do—right now—to reduce financial surprises.

Quick start: Pick your path

If you’re buying coastal property in Florida

- Get an insurance quote before you fall in love with the home

- Check flood zone status and elevation details early

- Budget for resilience upgrades and higher maintenance risk

If you’re buying inland

- Don’t assume “inland = safe” (rainfall flooding can still be costly)

- Review drainage, historical claims, and neighborhood flood patterns

- Build insurance + mitigation into your monthly payment plan

If you’re refinancing or renewing

- Re-run your payment comfort level including insurance increases

- Ask your lender how insurance/flood requirements affect underwriting

- Consider improvements that may help with insurability and risk

If you’re selling

- Gather proof of upgrades (permits, roof age, shutters/windows, elevation certificate)

- Be ready to answer “insurance and flood” questions early

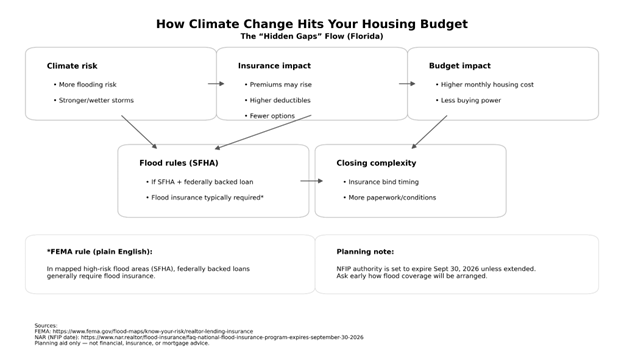

What “Climate Change” means for Florida housing in plain English

When people talk about the climate impact on Florida housing, they often picture a far-off future. But real estate reacts to what’s happening now—and what insurers, lenders, and buyers believe is likely.

In Florida, climate-linked risk typically shows up through:

- Rising sea levels (more frequent coastal flooding)

- Stronger or wetter storms (damage risk and repair cost)

- Flood exposure changes (maps, drainage limits, recurring water events)

- Insurance availability and pricing (affordability can change overnight)

- Lending and closing requirements (especially around flood insurance)

Think of it this way: Climate Change doesn’t have to “destroy” a neighborhood to affect home values. It can simply make a home more expensive to insure, harder to finance, or pricier to maintain.

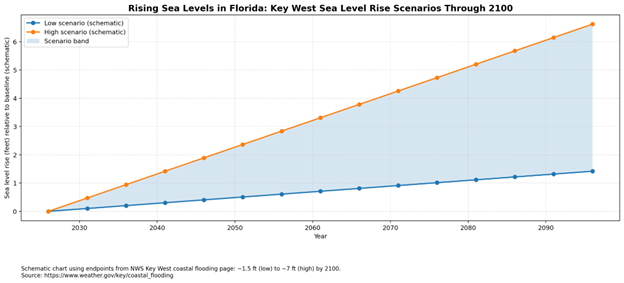

Rising sea levels in Florida: why it matters even on calm, sunny days

Sea-level rise isn’t only about dramatic storm surge. It can also raise the baseline water level so that “minor” high tides and rain events create more frequent nuisance flooding—including the kind locals call “sunny day flooding.”

For the Florida Keys, local sea level projections for Key West span a wide range by 2100—roughly 1.5 feet to about 7 feet, depending on the scenario.

What this means for you:

- A higher baseline sea level can make ordinary high tides more disruptive

- Drainage systems can struggle more often, even without a hurricane

- Homes that rarely flooded 20 years ago may see recurring issues now

Florida flood zone homes: why flood maps can change your mortgage and closing

Here’s the practical part many buyers learn too late: flood risk isn’t just a personal concern—it can be a financing requirement.

If a property is in a Special Flood Hazard Area (SFHA) and you’re using a federally backed mortgage, lenders are typically required to ensure flood insurance is in place.

So if a home is in an SFHA:

- Flood insurance may be required as a condition of closing

- Your monthly housing cost may jump compared to a similar home outside the SFHA

- Timing matters—if flood coverage can’t be bound quickly, the closing can be delayed

Hidden risk buyers miss: NFIP timing and uncertainty

Many Florida flood policies run through the National Flood Insurance Program (NFIP).

NFIP is currently authorized through September 30, 2026 (unless Congress extends/reauthorizes it). You don’t need to panic—but you do want awareness.

Why it matters:

- A lapse can create uncertainty for new policies/changes

- It can add friction to closing timelines in flood-prone areas

- It’s smart to ask early who will provide flood coverage and what backups exist

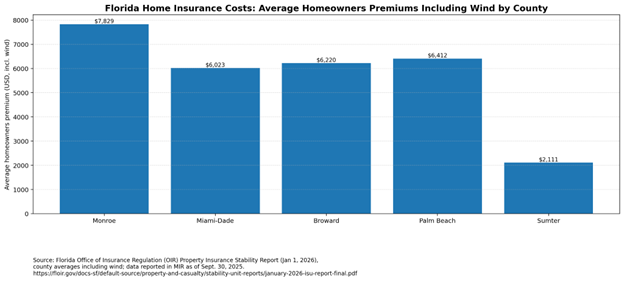

Florida home insurance costs: the affordability “gap” reshaping the market

In Florida, insurance is often the difference between a comfortable payment and a strained budget.

Florida’s Office of Insurance Regulation publishes county-level averages, and the spread can be dramatic.

Examples of average homeowners premiums (including wind coverage) reported in the January 1, 2026 Property Insurance Stability Report:

- Monroe: $7,829

- Miami-Dade: $6,023

- Broward: $6,220

- Palm Beach: $6,412

- Sumter: $2,111

Important: What you actually pay varies by insurer, coverage limits, insured value, deductibles, roof age, mitigation features, and claim history.

What this means for you:

- Two homes at the same price can have very different monthly costs once insurance is included

- Many buyers get payment shock after going under contract—because they shopped the list price, not the insurance cost

Why the Florida coastal property market is splitting into micro-markets

One of the biggest coastal trends in Florida is that the market is increasingly dividing into micro-markets.

Some neighborhoods show stronger resilience because they have combinations of:

- better elevation and drainage

- stronger building standards and newer roofs

- updated infrastructure

- better access to insurance options

Others feel more fragile because of:

- repeated flooding (even if it’s “minor”)

- fewer insurance carriers willing to write policies

- higher deductibles and stricter requirements

- rising maintenance costs and repair frequency

The hidden gap: county averages and general headlines can’t tell you what happens on one street versus another.

The new must-ask question

Instead of only asking, “Is this a good price?” also ask:

“Is this home affordable to own after I include insurance, flood requirements, and maintenance risk?”

What this means for mortgages and affordability

Here’s the clean way to think about it:

- A lender evaluates your ability to make the payment.

- Your real life includes the full housing cost: principal + interest + taxes + insurance + maintenance + (sometimes) flood insurance.

When climate risk pushes up insurance costs—or triggers required flood coverage—your budget can tighten even if the home price doesn’t change.

Common mistakes Florida buyers make right now

- Waiting until after the offer to request insurance quotes

- Assuming “not on the beach” means no flood risk

- Looking at list price only (ignoring total monthly cost)

- Skipping roof/permit/shutter documentation checks

- Not asking for claim history disclosures or repair records

- Treating flood zone status like a minor detail (it can affect lender requirements)

Step-by-step roadmap for buying smarter in Florida

1) Start with the payment you can live with

- Pick a comfortable monthly number (not just your max approval)

- Add a buffer for insurance changes and maintenance surprises

2) Shortlist neighborhoods with risk in mind

- Compare elevation/drainage patterns and proximity to water

- Ask locals/agents about recurring “sunny day” flooding on nearby roads

3) Check flood zone status early

- Confirm whether the property is in an SFHA

- Ask how that impacts flood insurance requirements and closing steps

4) Get insurance quotes before you commit

- Request homeowners (and flood if relevant) quotes before removing conditions

- Ask what could change the premium (roof age, mitigation features, prior claims)

5) Review the home’s “resilience file”

Mini-checklist:

- Roof age + permit documentation

- Impact windows/shutters

- Elevation certificate (if available/applicable)

- Drainage improvements (sump pumps, backflow valves)

- Prior water intrusion repairs + warranties

6) Align your mortgage strategy with risk reality

- Rate-hold timing and closing flexibility matter more when insurance is a variable

- If flood insurance is required, build the cost into both qualification and comfort budget

FAQ

Is Climate Change already affecting Florida real estate prices?

In many areas, it’s affecting the cost to own first (insurance, flood requirements, maintenance). Over time, ownership cost can influence demand and negotiating power.

Why are Florida home insurance costs so different by county?

Risk exposure and market conditions differ. Florida’s Office of Insurance Regulation shows large county-to-county differences in average premiums (including wind coverage).

What are Florida flood zone homes, and why do they matter for mortgages?

If a home is in an SFHA, federally backed loans typically require flood insurance as a condition of the mortgage.

If I’m not in a flood zone, should I ignore flood risk?

Not necessarily. Flooding can happen outside mapped high-risk zones. Some owners choose optional coverage, and some lenders may still ask additional questions depending on the loan.

What’s “sunny day flooding” and why should I care?

It’s minor coastal flooding that can occur with high tides—and it becomes more likely as baseline sea level rises. It can affect roads, drainage, and long-term upkeep.

Could NFIP issues affect closings?

NFIP authorization is set to run through September 30, 2026 unless extended. Changes or lapses can add uncertainty for new policies or modifications.

What’s one thing I can do this week to reduce risk?

Decide your all-in monthly budget and start collecting insurance quotes for any property you’re serious about—before you remove conditions.

Does “resilience” mean a home is “safe”?

No home is guaranteed safe. Resilience usually means the home/neighborhood is better prepared (construction, elevation, mitigation), which may reduce disruption and support insurability.

Wrap-up: the goal isn’t fear—it’s a smarter purchase

Climate Change is reshaping Florida real estate in a specific way: it creates hidden affordability gaps between homes that look similar on paper. In today’s market, the “winners” are often buyers who treat risk like a budget line item, because insurance, flood rules, and maintenance costs are now part of affordability.

Reminder: This article is general information, not mortgage, insurance, or legal advice.

If you’d like help pressure-testing a purchase budget (including insurance and flood requirements) and building a financing plan that fits your situation, talk to a licensed mortgage professional. A short conversation can help you avoid expensive surprises and buy with more confidence.