If you’re thinking about homebuying in Florida in 2026, you’re probably asking one big question:

“Do I actually stand a chance?”

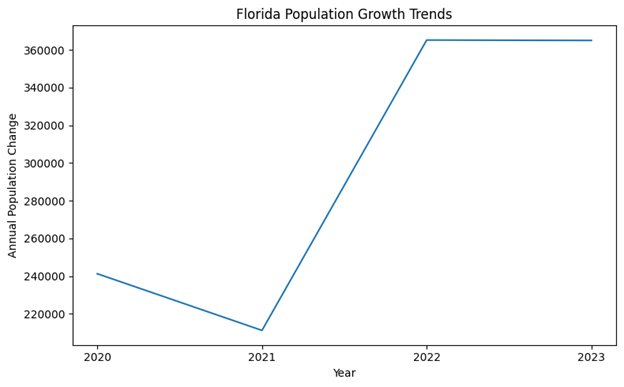

Between headlines about rising prices, bidding wars Florida buyers talk about, and interest rate uncertainty, it’s easy to feel like the deck is stacked against you. Here’s the reality: Florida remains one of the fastest-growing states in the country. Strong domestic and international migration continues to support housing demand. But here’s the good news.With the right preparation and structure, you can compete confidently, even in a competitive market.

Quick start: pick your path

If you’re just starting

- Review your credit and income

- Estimate your comfortable monthly payment (not just your max approval)

- Explore mortgage pre-approval Florida options

- Study recent price trends in your target area

If you’re actively shopping

- Get fully underwritten pre-approval (not just pre-qualification)

- Set your maximum offer number in advance

- Be ready to move quickly on strong listings

- Understand how to structure a competitive offer

If you’ve lost out on homes

- Reevaluate your offer structure, not just price

- Consider adjusting timelines or terms

- Explore nearby neighborhoods or property types

- Work with professionals who understand local competition

What’s really happening in Florida housing market trends (2026)

Three major forces are shaping Florida real estate right now:

- Continued population growth

- Higher mortgage rates compared to pandemic lows

- Regional supply differences

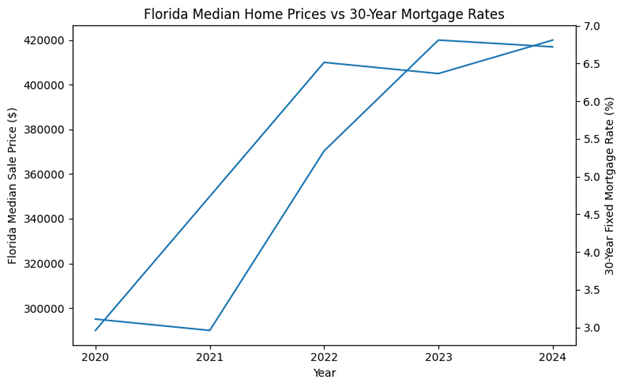

Mortgage rates rose significantly after historic lows in 2020–2021, cooling some of the extreme price spikes seen during peak demand years. At the same time, median prices in many Florida markets remain above pre-pandemic levels, though growth has moderated in some regions.

What this means for you:

- Some areas still feel like a seller’s market.

- Others are shifting toward balance.

- Micro-markets matter more than statewide averages.

Florida real estate competition hasn’t disappeared. It has evolved.

Why competition feels different in 2026

Florida attracts:

- Retirees

- Remote workers

- Investors

- International buyers

The state’s lack of a personal income tax continues to make it attractive for relocating households.

That demand creates pockets of bidding wars, especially in coastal areas, strong school zones, and move-in-ready homes.

But here’s what many buyers misunderstand:

It’s not always about offering the highest price.

It’s about presenting the strongest offer.

The power of mortgage pre-approval Florida buyers need

Let’s clear up confusion.

Pre-qualification = rough estimate.

Pre-approval = verified income, assets, and credit reviewed.

A stronger version, sometimes called fully underwritten pre-approval, means much of your file is reviewed before you make an offer.

In competitive scenarios, sellers often prefer:

- Buyers with verified financing

- Clean documentation

- Shorter financing timelines

- Clear communication from lender and agent

Strong financing signals reliability.

Building the strongest offer in Florida real estate

Price matters, but it’s not everything.

Sellers evaluate:

- Purchase price

- Financing strength

- Inspection period length

- Appraisal terms

- Closing timeline

- Earnest money deposit

Earnest money

Earnest money is a good-faith deposit submitted with your offer. Larger deposits can signal seriousness (funds are typically held in escrow and credited at closing).

Appraisal gap coverage

This means agreeing, within limits, to cover a shortfall if the home appraises below contract price. This carries risk and should be evaluated carefully.

The strongest offer is usually:

- Financially solid

- Clean and simple

- Confident but not reckless

Step-by-step roadmap to winning in 2026

1. Clarify your real budget

Factor in:

- County property taxes

- Homeowners insurance

- HOA fees (if applicable)

- Flood insurance (if required in FEMA-designated zones)

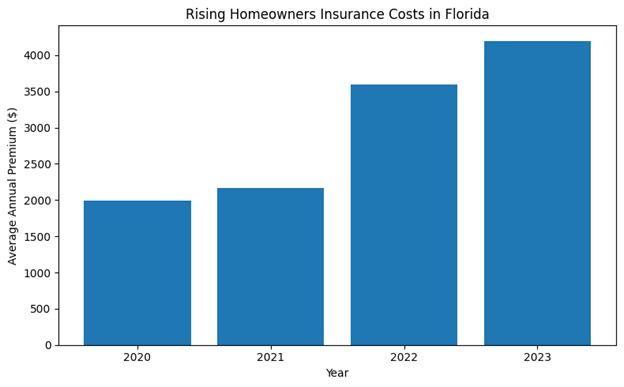

Florida insurance costs can vary significantly depending on location and risk profile.

2. Strengthen your credit profile

- Avoid new large debts

- Keep utilization low

- Make every payment on time

Even small improvements can impact pricing.

3. Secure strong pre-approval

Submit documentation early:

- Pay stubs

- W-2s or tax returns

- Bank statements

- Identification

Clarify:

- Down payment options

- Loan type (Conventional, FHA, VA, etc.)

- Estimated monthly payment range

4. Study micro-markets

Florida housing trends vary by:

- Metro area

- School zone

- Distance from coast

- New construction vs resale

Local data beats statewide averages.

5. Move fast, but stay disciplined

In competitive areas:

- Tour quickly

- Review disclosures carefully

- Submit strong offers promptly

But always stick to your pre-set maximum number.

Florida seller’s market strategies that actually work

When competition is strong, consider:

- Flexible closing dates

- Shorter (but reasonable) inspection windows

- Higher earnest deposits

- Clean, well-organized offer packages

What usually doesn’t work:

- Extremely lowball offers in hot areas

- Vague financing terms

- Last-minute changes

The goal isn’t to overpay.

It’s to be compelling.

Common mistakes that cost buyers the house

Shopping before speaking to a lender

This leads to weak offers and missed opportunities.

Ignoring insurance costs

Florida homeowners insurance costs have risen in recent years due to storm risk and insurer market changes. Failing to estimate insurance early can derail deals.

Waiving protections blindly

Waiving inspections or appraisal contingencies can expose you to expensive surprises—especially in hurricane-prone areas.

Letting emotions take over

Bidding wars can feel personal. They’re not.

Set your limit. Respect it.

FAQ

Is 2026 a good year for homebuying in Florida?

It depends on your finances and location. Some areas remain competitive; others are balancing.

How do I win a bidding war?

Strong pre-approval, clean terms, and disciplined pricing matter more than emotion.

Are bidding wars still common?

In certain price ranges and desirable neighborhoods, yes. In others, competition has softened.

How much earnest money is typical?

Often 1–3% of purchase price, though norms vary by market.

What about flood insurance?

If the property is in a designated flood zone, lenders may require flood insurance. Costs vary by risk level.

Should I wait for rates to drop?

Rates fluctuate based on broader economic conditions. The right timing depends on your budget and long-term plan.

The bridge: why professional guidance matters

Online advice often focuses on “offer more money.” But in real-world Florida real estate competition, structure matters just as much as price.

The nuance, inspection timing, appraisal terms, lender communication, insurance estimates, can make or break a deal.

Working with professionals who understand local conditions can help you:

- Identify realistic offer strategies

- Avoid unnecessary risk

- Stay disciplined under pressure

Final thoughts on homebuying in Florida (2026)

Homebuying in 2026 doesn’t require luck. It requires preparation.

When you understand:

- How to structure the strongest offer

- How mortgage pre-approval strengthens your position

- Which seller’s market strategies actually work

You move from anxious to confident.

Ready to build your strategy? Book a homebuying strategy session. We’ll review your budget, pre-approval strength, target neighborhoods, and offer structure, so you can compete without overextending yourself.